Volatility Is Back. Our View Has Not Changed.

By Tucker P. Nicholas, Private Wealth Advisor at PAC Financial, Harrisburg, PA. July 17, 2026.

Markets had a rough week, especially in technology and semiconductor names. Several of you have called or emailed asking what we think. Fair question. Here is our current view from the office, in plain English. This is general commentary, not personalized advice, and these are our opinions as of today, not a recommendation to buy or sell any security.

What actually happened this week

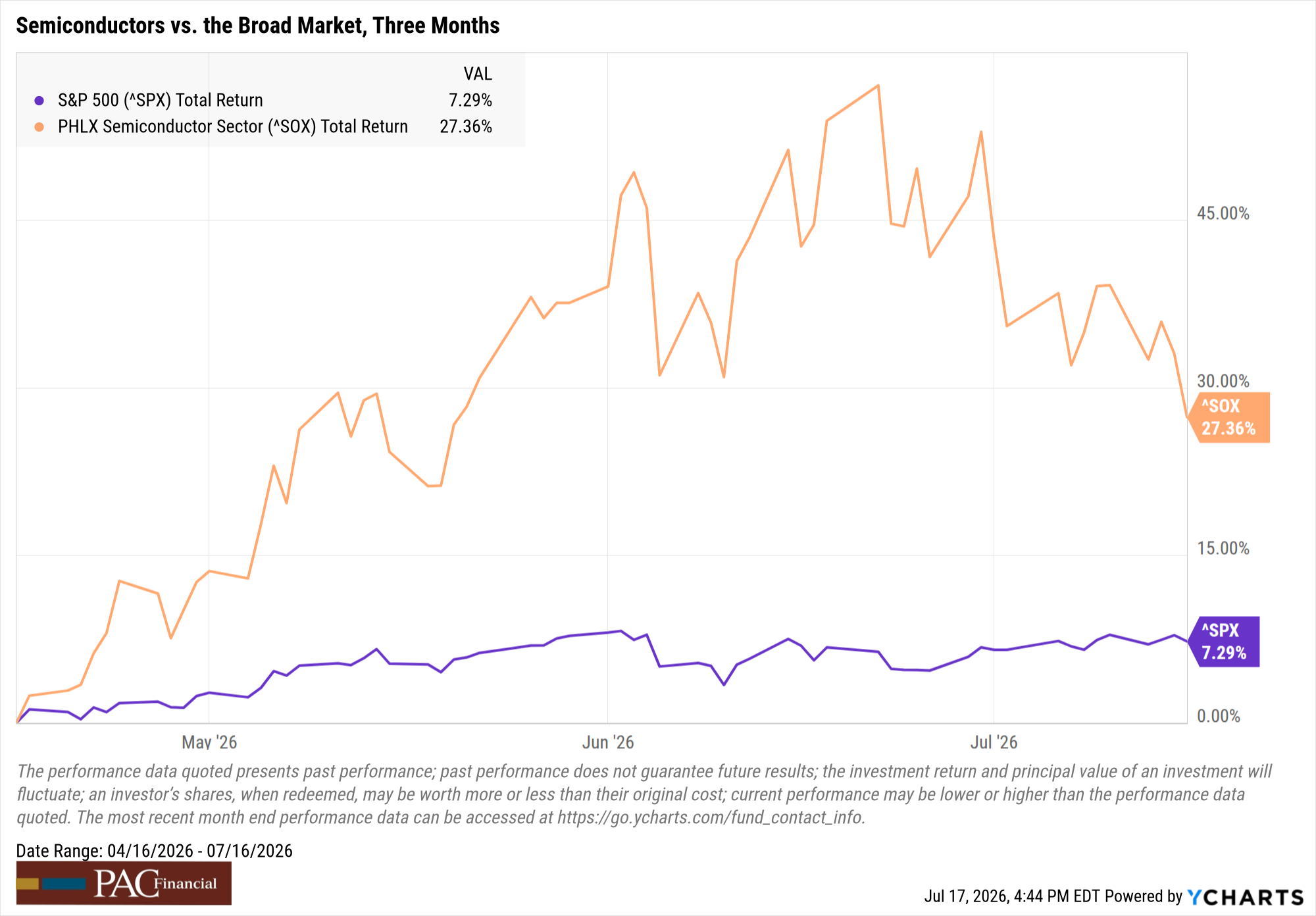

Stocks sold off in the quiet stretch between earnings seasons, with the sharpest moves in chip and memory names. Here is the part we keep coming back to: the underlying earnings picture has not changed this week. Last quarter, leading memory and chip manufacturers reported results ahead of analyst estimates, and we are not aware of any major company in the space revising its outlook downward this week. Prices moved. The reported fundamentals did not.

One more mechanical factor worth naming: today, July 17, was monthly options expiration. On expiration days, contracts tied to stocks and indexes expire, and traders adjust or unwind hedged positions all at once. That process often adds selling pressure that has nothing to do with any company's business, and this month it landed right on top of the Korean margin-call story. Neither one is a change in the earnings picture.

When prices move faster than facts, we ask questions about the selling before we question the companies.

The Week by the Numbers

| Index | This Week | Year to Date |

|---|---|---|

| S&P 500 | -1.55% | +8.43% |

| Nasdaq Composite | -2.9% | +9.8% |

| Dow Jones Industrial Average | -0.93% | +8.5% |

| Russell 2000 | -0.52% | +19.35% |

| PHLX Semiconductor Index | -9.97% | +64.81% |

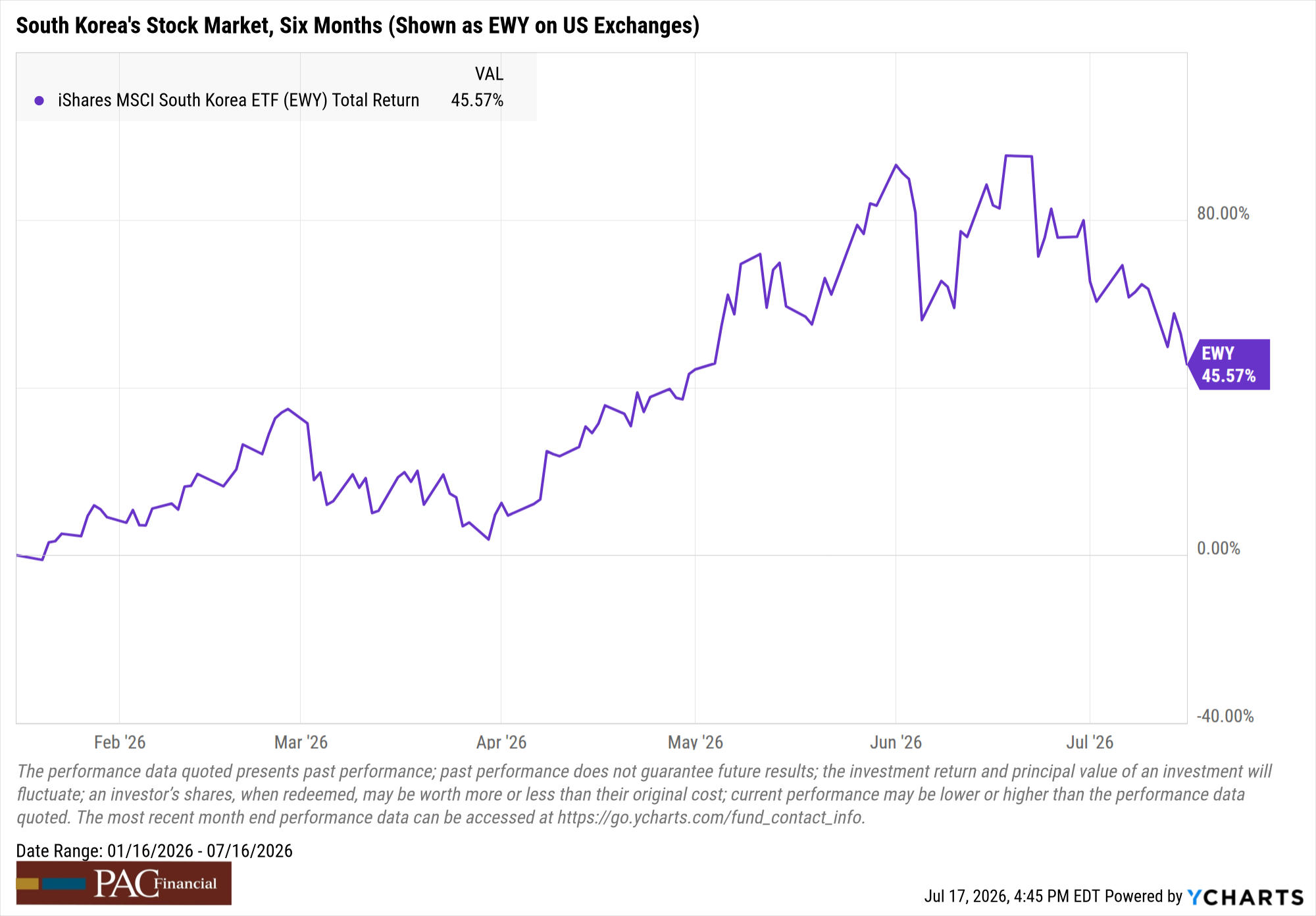

| KOSPI (South Korea) | -5.86% | +61.85% |

| Rates & Economic Data | Latest | Context |

|---|---|---|

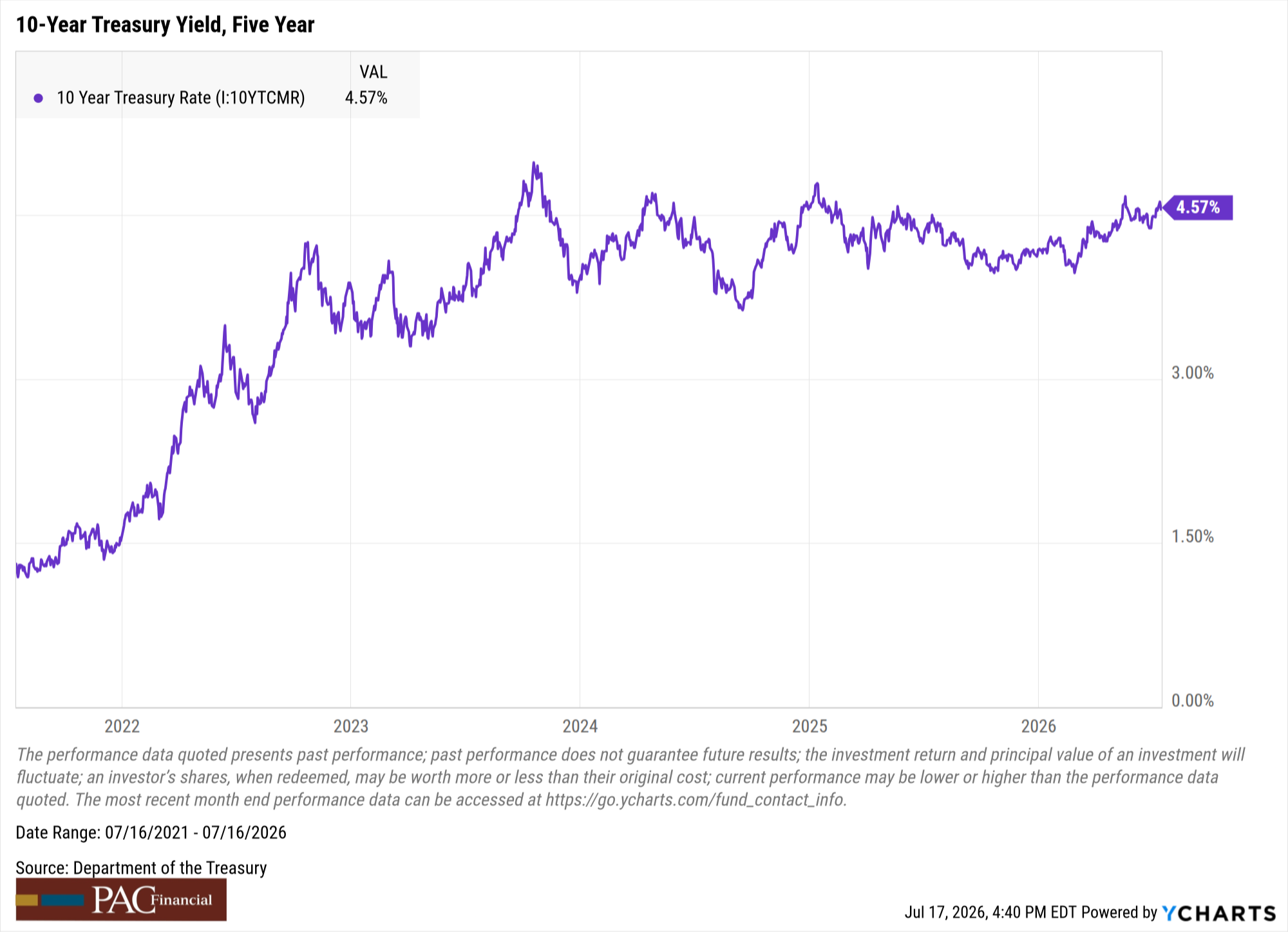

| 2-Year Treasury Yield | 4.16% | last week 4.21% |

| 10-Year Treasury Yield | 4.57% | last week 4.56% |

| 30-Year Treasury Yield | 5.09% | last week 5.06% |

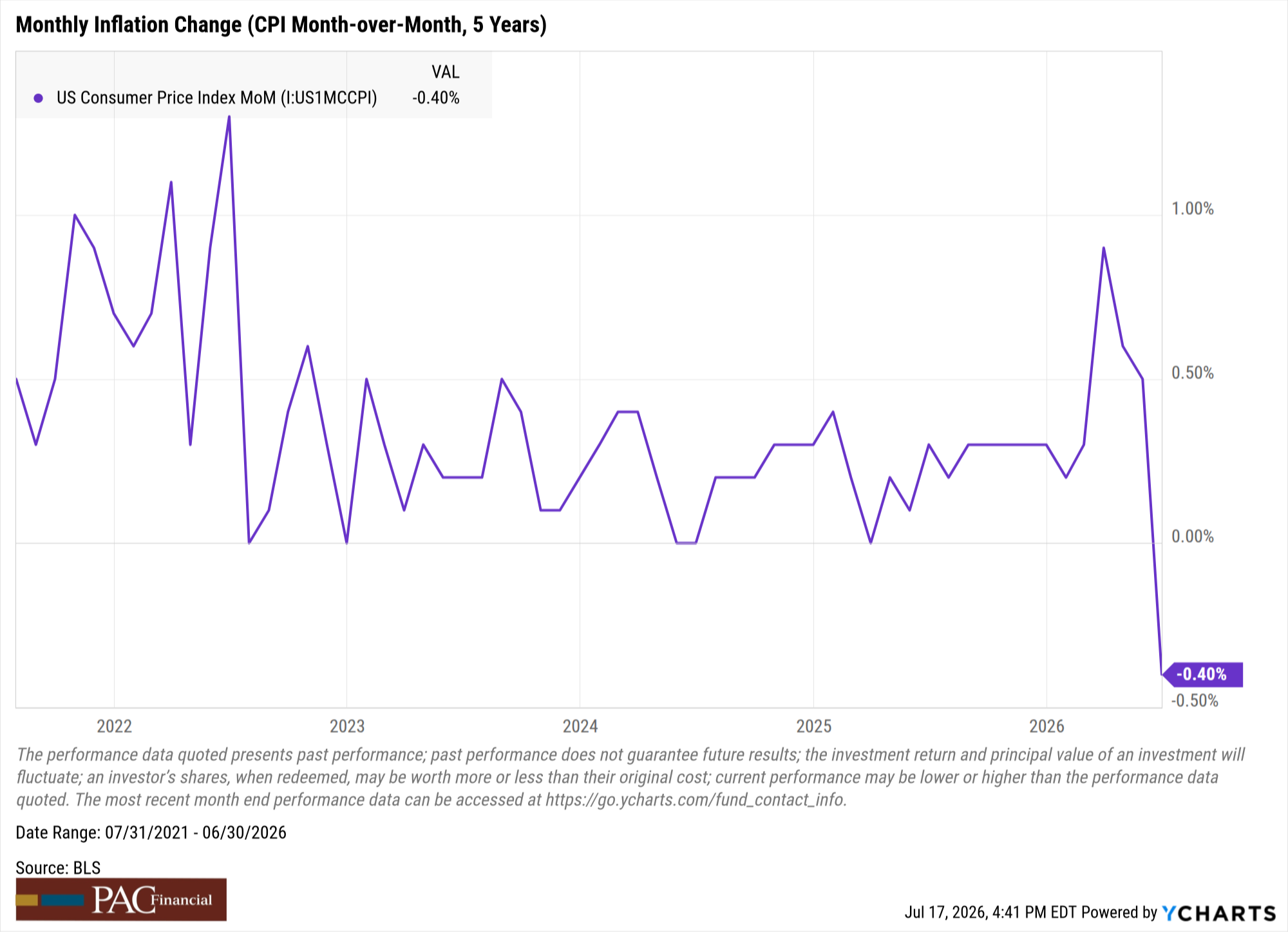

| CPI, Month over Month (June) | -0.4% | largest monthly decline since April 2020 |

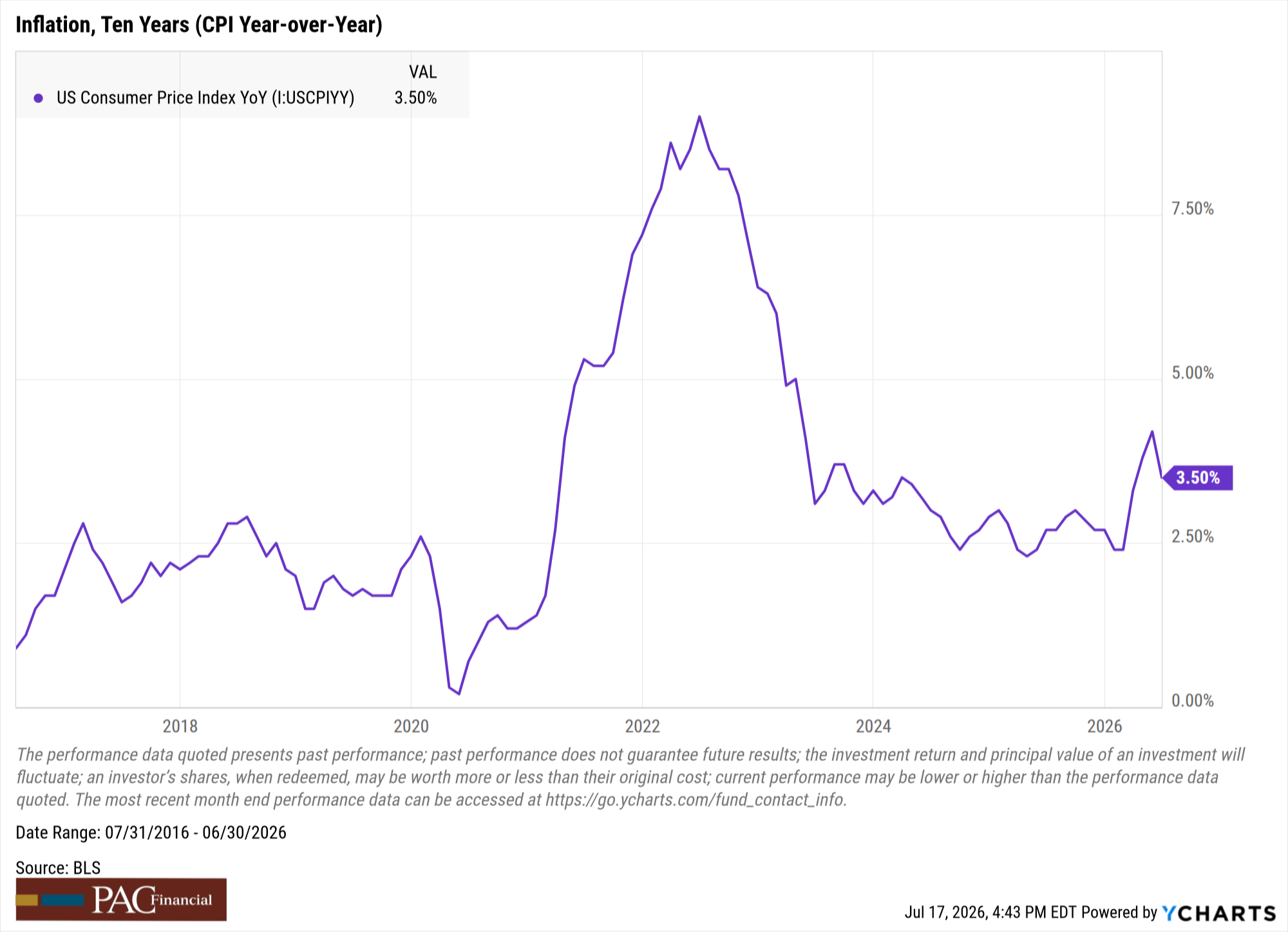

| CPI, Year over Year (June) | 3.5% | below the 3.8% consensus |

| Core CPI, Year over Year (June) | 2.6% | excludes food and energy |

| PPI, Month over Month (June) | -0.3% | consensus expected flat |

| Weekly Jobless Claims | 208,000 | down 8,000; historically low |

| Fed Funds Target Range | 3.50–3.75% | unchanged since June 17, 2026 |

Index data as of market close, July 17, 2026. Treasury yield data as of July 16, 2026, the most recent available at publication. Sources: YCharts, U.S. Bureau of Labor Statistics, U.S. Census Bureau, Federal Reserve. Indexes are unmanaged and cannot be invested in directly. Index performance is shown for illustration and does not represent any PAC Financial client account.

The Korea connection

Some of this week's turbulence traces back to South Korea, which has been the world's best performing major stock market this year. This week the Bank of Korea raised its policy rate to 2.75%, its first hike in over three years.

Headlines treated the hike as a scare. We would offer a different way to read it. Central banks generally raise rates when they judge an economy strong enough to no longer need help. Korea sits at the center of the global memory and AI buildout, and that buildout has been a major contributor to Korean exports and growth this year. Seen through that lens, the first hike in three years reads less like a warning and more like a statement of confidence: in our view, policymakers looked at an economy running hot and concluded that emergency-level support was no longer necessary. And 2.75% is still a moderate rate by historical standards.

The hike did have a mechanical side effect, and that is what markets felt first. Leveraged trading had become widely popular with Korean retail investors on the way up. Higher rates raised the cost of carrying those positions, the unwinding began, and margin calls forced waves of selling. Because Korea is home to some of the world's biggest memory chip makers, that forced selling spilled into the same global names our clients ask about most.

iShares MSCI South Korea ETF (EWY), used as a U.S.-listed proxy for Korean equity performance and shown for illustration only. Source: YCharts.

Forced selling reflects the seller's circumstances. It says little about the business being sold. We treat those as two different pieces of information.

Is this the dot-com bubble all over again?

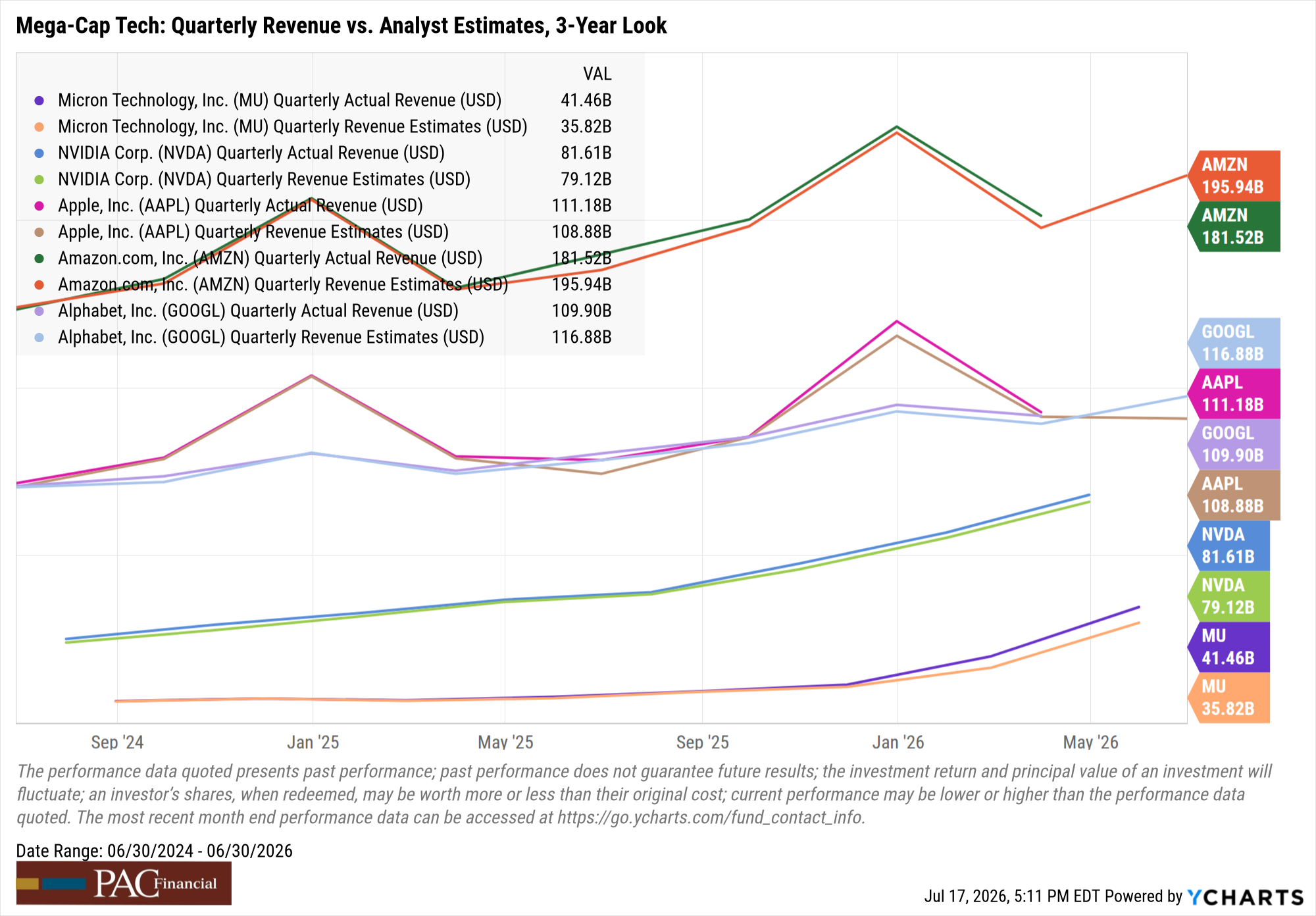

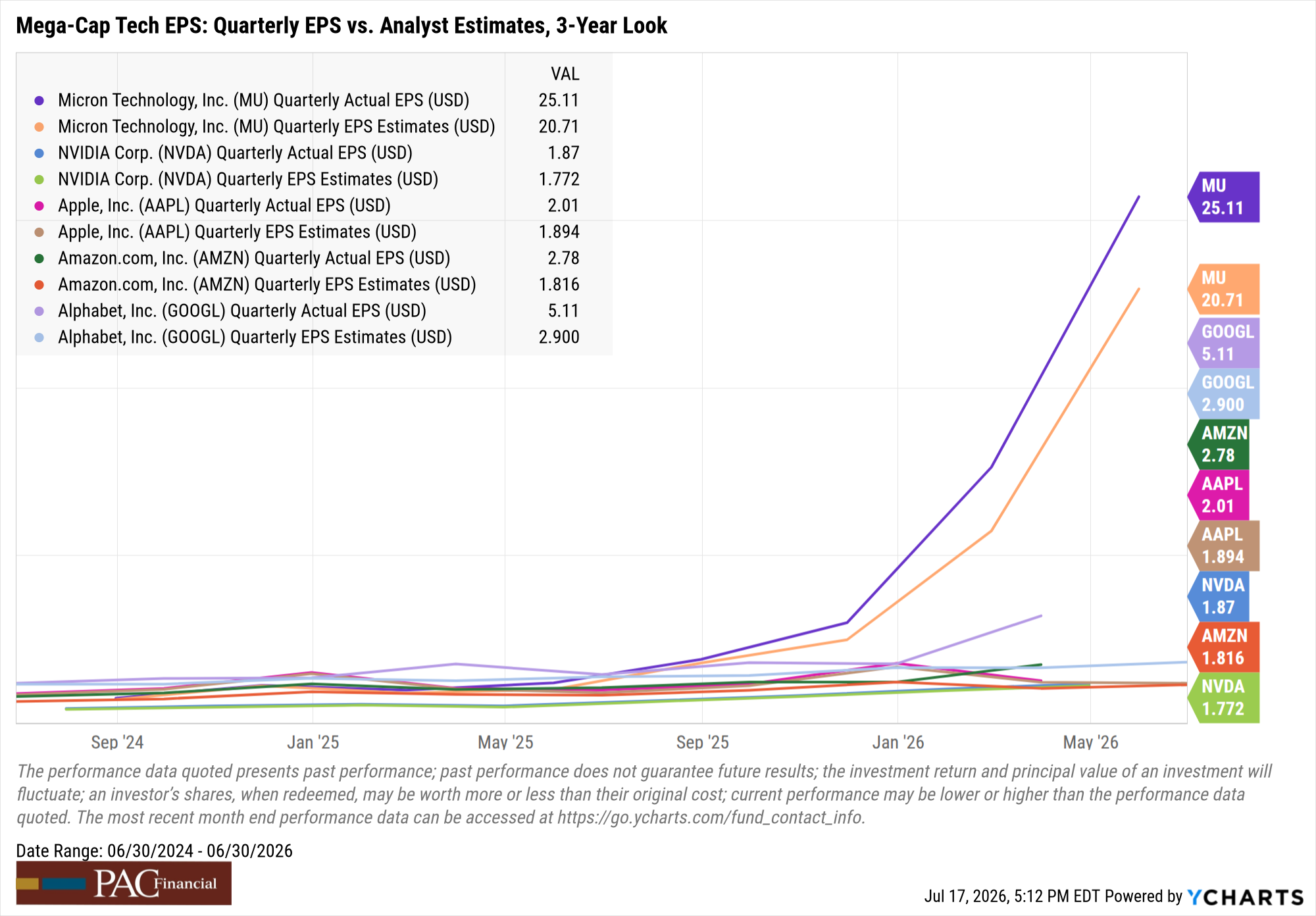

A few of you have asked this directly, and it deserves a direct answer. In our view, no, and the difference is visible in the financial statements.

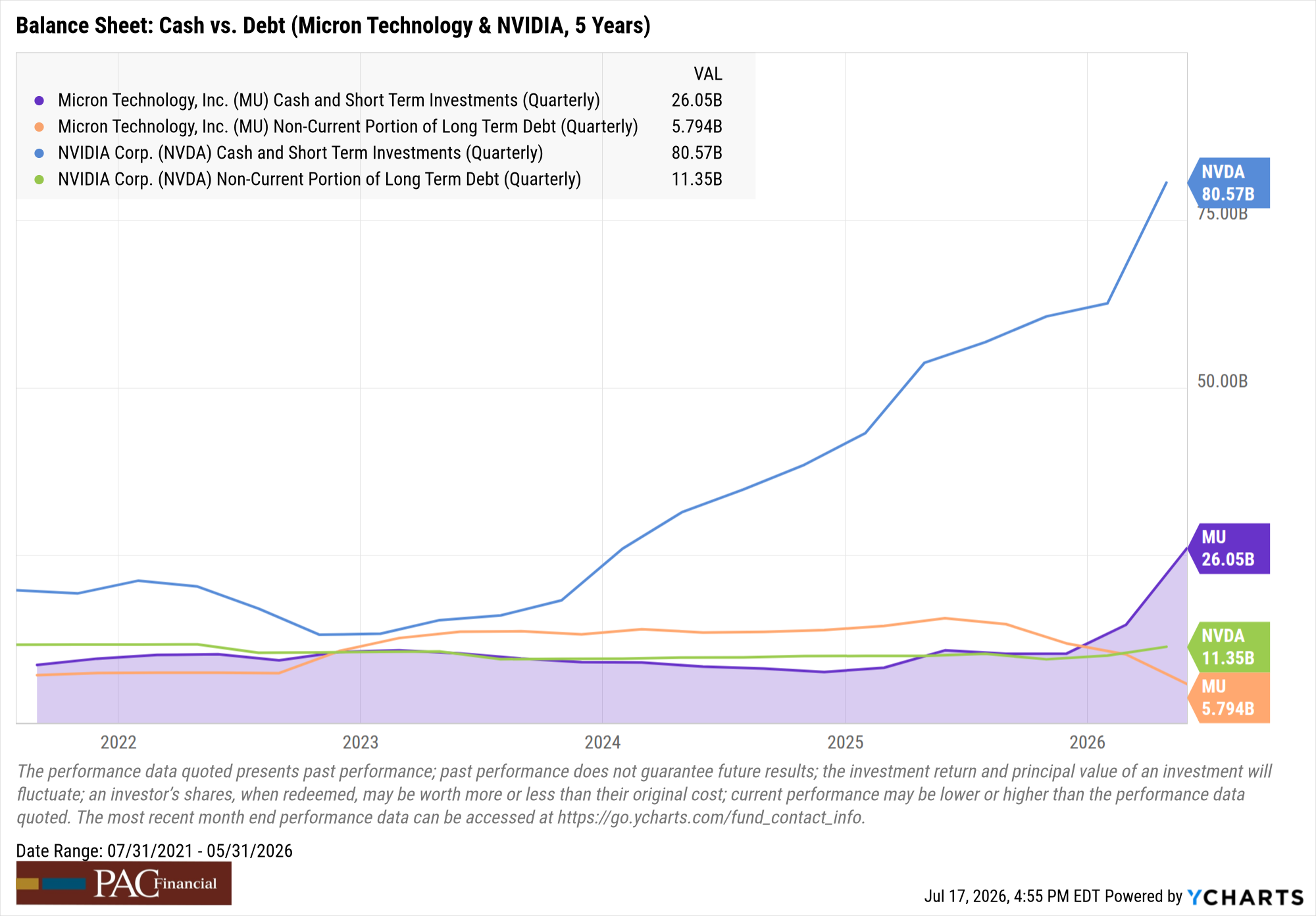

In 1999 and 2000, the market's hottest companies were priced on website traffic and big promises. Many had little revenue, no profits, and burned borrowed money to stay alive. Today's technology leaders are a different animal. They are reporting record revenues and profits, beating analyst estimates quarter after quarter, and funding the AI buildout largely out of their own operating cash flow rather than debt. The balance sheets carrying this buildout are among the strongest in corporate America.

Company data shown for illustration of sector fundamentals only and is not a recommendation to buy or sell any security. PAC Financial clients may hold positions in securities shown. Source: YCharts.

None of this means prices cannot fall, and it does not mean valuations are cheap. It means the foundation under this market is reported earnings rather than speculation, and that is the structural difference we weigh when we distinguish this week's volatility from something more serious.

On inflation and the Fed

This week's inflation data deserves a careful read, because the headlines blurred it. Tuesday's Consumer Price Index report showed consumer prices fell 0.4% from May to June, the largest single-month decline in over six years, driven largely by a 5.7% drop in energy prices. That pushed the annual inflation rate down to 3.5%, below the 3.8% economists expected. Core inflation, which strips out food and energy, ran at 2.6% for the year. Wednesday's Producer Price Index report added to the picture: wholesale prices unexpectedly fell 0.3% for the month, with goods prices posting their sharpest drop in nearly two years.

The rest of the week's data showed an economy cooling, not cracking. June retail sales rose, and once you strip out falling gasoline prices, spending jumped 0.7%. Weekly jobless claims fell to 208,000, a historically low level of layoffs. Taken together, it was a balanced week of data: cooling inflation alongside steady spending and a resilient labor market.

The bond market appears to be reading it the same way. The 2-year Treasury yield, the maturity most sensitive to Fed expectations, fell from 4.21% to 4.16% this week, and the long end barely moved. That is not what rate-hike fear looks like.

We continue to monitor the Federal Reserve's rate path for 2026. In our opinion, the market's rate-hike fears currently sit ahead of what this week's data shows. We hold that view loosely: if the data changes, our view will change with it.

On China and the AI race

The latest Chinese AI model release, Kimi-K3, stirred fears that China is pulling ahead. We would note that the U.S. government has stated, repeatedly and across administrations, that leadership in AI is a national security priority. We believe that policy backdrop continues to support American companies involved in the AI buildout, and in our view this buildout has a runway measured in years, not quarters. One competitor's model release does not, by itself, change the capital already committed.

A word about election years

This is a midterm election year. Midterm years have historically been choppier than average for markets. We expected volatility coming into 2026 and we expect more of it before November. That is normal, and it is manageable with a plan.

What could change our view

Honesty requires naming the other side. Our outlook would get more cautious if the coming earnings season disappoints at quality companies, if inflation re-accelerates and puts rate hikes back on the table, if geopolitical tensions escalate in ways that disrupt supply chains, or if the leverage unwinding abroad spreads into broader forced selling. We watch all four. None of them is our base case today.

Where we land

In our view, this week's selling looks disconnected from the reported earnings data. Until the earnings picture changes at good companies, our forward outlook remains constructive despite short-term swings. History also suggests that reacting emotionally to short-term declines has often done more damage to long-term plans than the declines themselves. Whether any of this calls for action in your accounts depends on your plan, your timeline, and your situation. That is a conversation, not a blog post.

If this week rattled you, or if you want to review how your accounts are positioned, call us. That is what we are here for.

One more thing: Trump Accounts are in the news

We have started receiving calls at the office from families who read about the new Trump Accounts and want to learn more. Since July 4, these accounts are open for contributions, and the federal government offers a one-time $1,000 contribution for eligible children born 2025 through 2028. If you have kids or grandkids in that window, we wrote a plain-English guide that covers eligibility, the $5,000 annual limit, the employer contribution option, and how the accounts are invested: Trump Accounts at PAC Financial. It is worth ten minutes of your time.

New to PAC Financial?

Some of the people reading this found us through a search engine or a friend, not through an account with us. Welcome. If you do not currently work with a financial advisor and want one steady voice through this volatility, or you want help understanding Trump Accounts for your family, we are taking new client conversations. The first meeting is about your goals and your questions, not a sales pitch. We are a third-generation independent firm at 5291 Devonshire Road in Harrisburg, working with families across Pennsylvania in person or by video, and virtually with residents of other states where we are registered.

Stephen A. Marrazzo

Financial Advisor

T: (717) 564-6400 ext 104

E: smarrazzo@osaicwealth.com

Tucker P. Nicholas

Private Wealth Advisor

T: (717) 564-6400 ext 181

E: tnicholas@osaicwealth.com

Compliance Notice

The opinions expressed are those of the authors as of the date of publication and are subject to change without notice. This material is for informational purposes only and is not personalized investment advice, nor a recommendation or an offer or solicitation to buy or sell any security. Any securities or company data shown are for illustration only. Forward-looking statements are not guarantees of future results, and actual events may differ materially. Investing involves risk, including the possible loss of principal, and no strategy assures success or protects against loss in a declining market. Past performance is no guarantee of future results. Indexes are unmanaged and cannot be invested in directly. International investing involves additional risks, including currency fluctuation and political and economic instability. Exchange-traded funds are shown for illustrative purposes only. Trump Accounts are governed by Public Law 119-21 and 26 USC Section 530A; rules and eligibility are subject to change, and PAC Financial does not establish or administer Trump Accounts. Economic and market data are drawn from sources believed to be reliable, including YCharts and public government releases, but accuracy and completeness are not guaranteed. Securities and advisory services offered through Osaic Wealth, Inc., member FINRA/SIPC. PAC Financial and Osaic Wealth are separately owned and other entities and/or marketing names, products or services referenced here are independent of Osaic Wealth. Check the background of your financial professional on FINRA's BrokerCheck.